As part of the ongoing effort to bring financial literacy to more middle class families, a regular bit of advice given out is that it is necessary to teach our children how to open a bank account and save money, pay bills, etc. While that is a good lesson to learn, it is not complete. It only focuses on one side of the equation. We forget about the bank itself, and how they make tons of money at our expense.

There’s an expression that the best way to rob a bank is to own one. Banks, like any other capitalistic company, are in the business of turning a profit by any means necessary. And if they have investors on Wall Street, they have to cater to them, usually at the expense on regular account holders.

What does this mean really?

In a nutshell, it means they won’t pay you when they make a profit on the money in your account. Banks lend your money and profit on the interest, and invest your money, flipping it in the stock market and earning dividends, yet charging you a slew of fees.

Now you see why I wrote that quote about the best way to rob a bank?

In a fair investment partnership, each partner share in the profit based on the percentage of their investment. Likewise, each bank account holder should be treated as an investment partner, but it penalized like a slave instead.

You might say, “well, I get it. But that’s just how banking is. I still think it’s necessary to teach our children how to open accounts and save money.” Fair enough. Saving money is not a bad thing, but not understanding how banks hold and guarantee that money is another. Try an experiment. If you have several thousand dollars in your account right now, try to ask for all of it in cash. Let’s assume you have $5,000. Are you confident you will get all of that in cash? Wanna bet?! What’s going to happen is that the bank may give you $1,500 or even $2,000, and the rest in a cashier’s check.

Why?

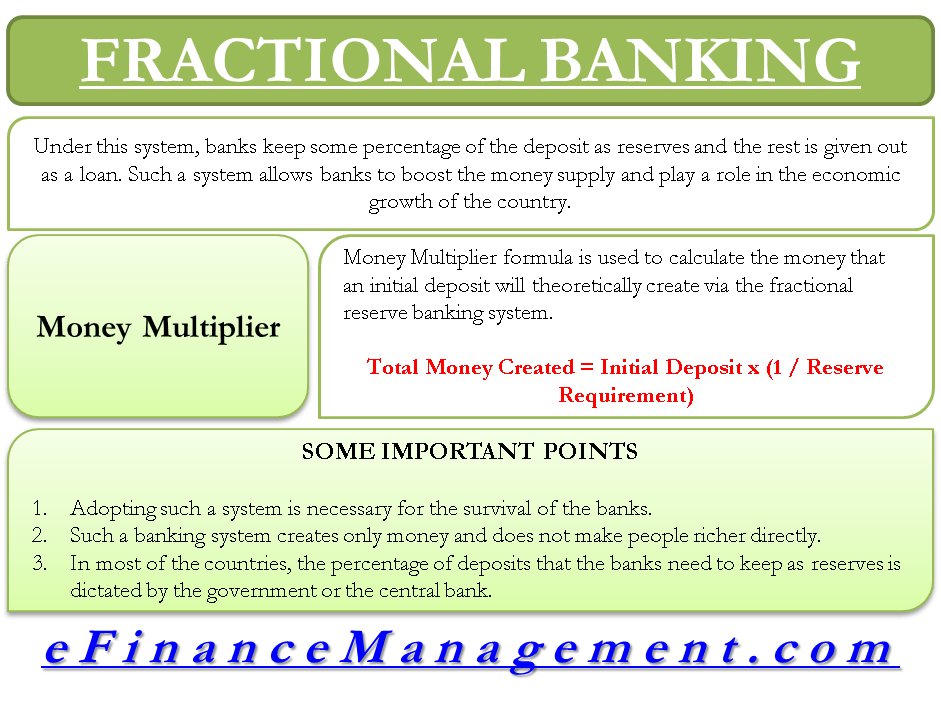

Because once we moved off the gold standard long ago, we no longer have the relatively consistent, intrinsic value of a precious metal backing up the paper currency. As a result, bank regulators mandated each bank have a certain percentage of cash on hand to guarantee all depositors can get their money out on demand. How does this work? [Continue after image]

Let’s say your bank has 10 accounts for 10 customers, $10,000 per account. The total of all deposits is therefore $100,000. If the reserve requirement is 20%, that means the bank has to have $20,000 in cash available to give to customers who want to withdraw money. (For all the bank nerds out there, lol, I’m just keeping this example simple without getting bogged down in technical details). This kind of reserve requirement has worked for some years without any widespread runs on the bank (where every customer demanded all their money at once).

Over time, however, the reserve requirement this percentage decreased without a lot of press coverage. Most banks barely carry enough cash to meet all their customers demands. it is not known exactly how much cash each bank has on hand, but a worldwide formula has sought to encourage banks to maintain something like 2.5% to 7% (click the link for more details on the formula). Based on my past research, the rate for U.S. banks might be hovering around 2 to 3%. Using our example again, at 2%, this means that the bank likely only has $2,000 cash on hand at any time to give to customers for withdrawal.

This is why you’d be surprised that your bank can’t give you a lot of cash if you try a big withdrawal. Consider this a big wake up call if you took you bank account for granted. A bank that cannot guarantee full services to its customers should be looked at with scrutiny. And the FDIC system, which supposedly guarantees all accounts up to $250,000, should be looked at given that the government backing it up is now over $21 trillion in debt. It can find money for wars but not enough to make you a true partner of your bank.

What are you options besides stuffing what little money your bank gives you under your mattress? Investment clubs are popular, where like minded individuals pool their money together to buy various stocks, bonds and other investment products to flip their money much better than bank accounts can. These require some research to make the right decisions. When it comes to spreading financial literacy to children, teach them about opening investment accounts and starting investment clubs for those who don’t have enough money on their own. Just make sure the relationship can survive any disagreements about terms and conditions down the road.

If you have enough of your on money to invest without a club, that’s even better. Buying stocks is much cheaper these days. TD Ameritrade charges about $6 per trade ($6 when you buy one or more stocks, and $6 when you sell the same stocks later). There are several online trading sites to explore. The objective of this article is to make you aware of the fact that your bank account is not to be taken for granted, and that there are developments underway in the world where your money may be at risk soon. It is good to teach our children the complete story about bank accounts and savings, and to know that the bank is not just sitting on the money, but making a ton of money at your expense, and cannot guarantee it can give you all your money in cash if you ask for it. Think of your savings as an investment opportunity, not simply a piggy bank for the bankers to profit form.